Gold & LSE Gold Miners: Integrated Framework – Amplified Pullback in a Secular Bull (28 June 2026)

Gold has traced a powerful secular advance from the 2022–2023 lows to a January 2026 high above $5,600 before correcting sharply into the current $4,087–$4,473 zone. The daily chart shows a breakdown with lower highs and price testing Fibonacci retracements of the breakout alongside a rising trendline, with RSI dropping to a 2 year low in mid June. What is encouraging is we briefly dipped below 4,000, checked, and then recovered. We've also stayed within my consolidation line on the daily. This is a key area to watch and, for me, remains the line in the sand in terms of building and adding to positions. By using trailing stops and scaling in, this allows us to shadow the continuation of the trend and offers the possibility that these can then become longer term positions assuming the uptrend continues but, at worst, they become trades if it reverses and you become stopped out off a trailing stop.

The weekly(see below) and monthly gold futures charts preserve the higher-timeframe uptrend structure.

Last year in April i did a study on gold cycles which suggested this cycle should run to 2027-2028 with a high around $5500 to $6000 (See HERE) . This current article sets out the bull and bear case for whether indeed we have now seen the end of the trend or if this is a pullback within a broader uptrend. I've considered both the bull and the bear case and then below this is the article following on from the seasonality and cyclicality of gold, which looks at the differential response to some of the more liquid UK gold miners to movements in the underlying.

Combined this gives us a framework to trade in, whilst observing some of the key levels to understand whether we should be invested or not. That will become clearer with time.

So, in summary, we're pulling together three elements in this:

- The broader secular bull market in gold, which I covered last year - HERE

- The seasonality that we see within gold every single year and have done over the past 26 years that I looked at. We're clearly in that seasonal June swoon - HERE

- The opportunities to trade responses within the precious metal miners in the UK markets, so we can make some money recognising the influence of 1) and 2)

The recent moves in high-beta LSE/AIM gold miners have been materially larger than gold’s own correction. This analysis integrates the gold macro and technical picture with miner-specific beta, liquidity, fundamentals, and seasonal behaviour, while incorporating the operational and macro factors that have amplified the pullback.

The conclusion is that this is a tough but explainable correction within an ongoing structural bull, not the bend at the end of the trend ( I think!) The broader 26 year study on gold seasonality forms Part 1 of this series .

The Gold Miner report below this articles is generated by the ACE agentic research team and will be updated with prices end of day EVERY day. It clearly shows the seasonality of the price advances in the UK gold and precious metals miners. These are amplified by other features like the strength in gold we've seen recently, like the increase in oil prices, and are compounded by the fact that some of these companies are in different stages of mine development. That will skew the AISC costs and therefore the price response is a function of margin compression while they are in these early stages of mine development. All that been said in a cyclical business you tend to get an over capacity situation occurring near the end, in other words a lot more investment in mines. It plays back to the question mark about whether we are seeing the final throes of the much bigger secular cycle.

1. Gold Macro & Technical Context

The higher-timeframe structure remains bullish. Weekly and monthly charts show intact higher highs and higher lows since the prior base. The daily correction is sharp and has broken near-term trendline support, but it is landing on Fibonacci retracement zones consistent with healthy pullbacks in prior cycles.

Bull case: Structural central bank demand (244 tonnes net in Q1 2026, tracking toward 750–1,100 tonnes annually) provides a price-inelastic floor. The post-pandemic regime has rebased gold to a higher range, with $4,000 increasingly viewed as the new baseline. Seasonal timing (late June) aligns with the historical accumulation window ahead of stronger Aug–Sep and Dec–Jan periods. Institutional forecasts generally see consolidation or grind higher toward $4,500–$5,200 by year-end, with upside to $5,400–$6,000+ on eventual Fed easing.

Bear case: The January 2026 high carried parabolic characteristics followed by lower highs. A sustained break below the $4,000–$4,115 confluence would open deeper measured-move targets. Near-term macro headwinds (stronger USD, elevated real yields) remain active.

Early in the year gold became memetic — aggressively chased in a manner reminiscent of crypto-style retail and momentum flows. That hype phase has clearly soured. Sentiment has turned, capital has rotated toward new shiny objects, and the marginal buyer has stepped back. Gold yields nothing, creating a material opportunity-cost problem in an environment where duration concerns are rising and real yields remain elevated for longer than many expected. If the US dollar is transitioning from a cyclical high into a secular uptrend, it becomes a persistent structural headwind rather than a temporary one, capable of capping gold’s upside and amplifying downside pressure for an extended period.

In this scenario the recent correction is not merely a healthy pullback but the start of a more prolonged de-rating. High-beta miners would face further multiple compression as the hype premium evaporates and operational realities (elevated AISC, development costs, energy inflation) are scrutinised more harshly. A sustained break below the $4,000–$4,115 confluence on gold would likely trigger another leg lower in the miners, with limited immediate support until sentiment and macro conditions improve

Assessment: The weight of evidence favours a cyclical correction rather than a confirmed cycle top. The daily oversold condition and seasonal context create a constructive setup for stabilisation, provided key supports hold. BUT we we remain mindful of the parameters that define the bear case and have a way to characterise that but ultimately the line in the sand becomes the arbiter. Does gold hold?

2. Macro & Operational Headwinds Explaining Recent Amplification

Several concurrent factors have magnified the recent drawdown in gold miners beyond a simple beta multiple of gold’s move:

- Mine development and maturity stage. Early-stage build-outs and expansions carry elevated AISC. For Hochschild, the Mara Rosa project is in the bedding-in phase where unit costs are structurally higher before efficiencies scale. For Pan African, ongoing expansion into new areas/franchises adds upfront costs that are expected to normalise as operations mature. This is normal operational leverage in the development cycle, not a permanent impairment.

- Energy cost spike. Oil has risen sharply, directly feeding into higher diesel and energy expenses. Energy is a major component of mining and exploration costs; the pass-through has contributed to short-term AISC pressure across the sector. Given oil prices have eased fairly spectacularly in the past month, this should directly transfer to lower production costs and therefore reductions in the AISCs, which brings margin improvement.

- Stronger USD. A firmer dollar has weighed on gold and therefore on beta-sensitive miners, adding a macro overlay to the de-rating.

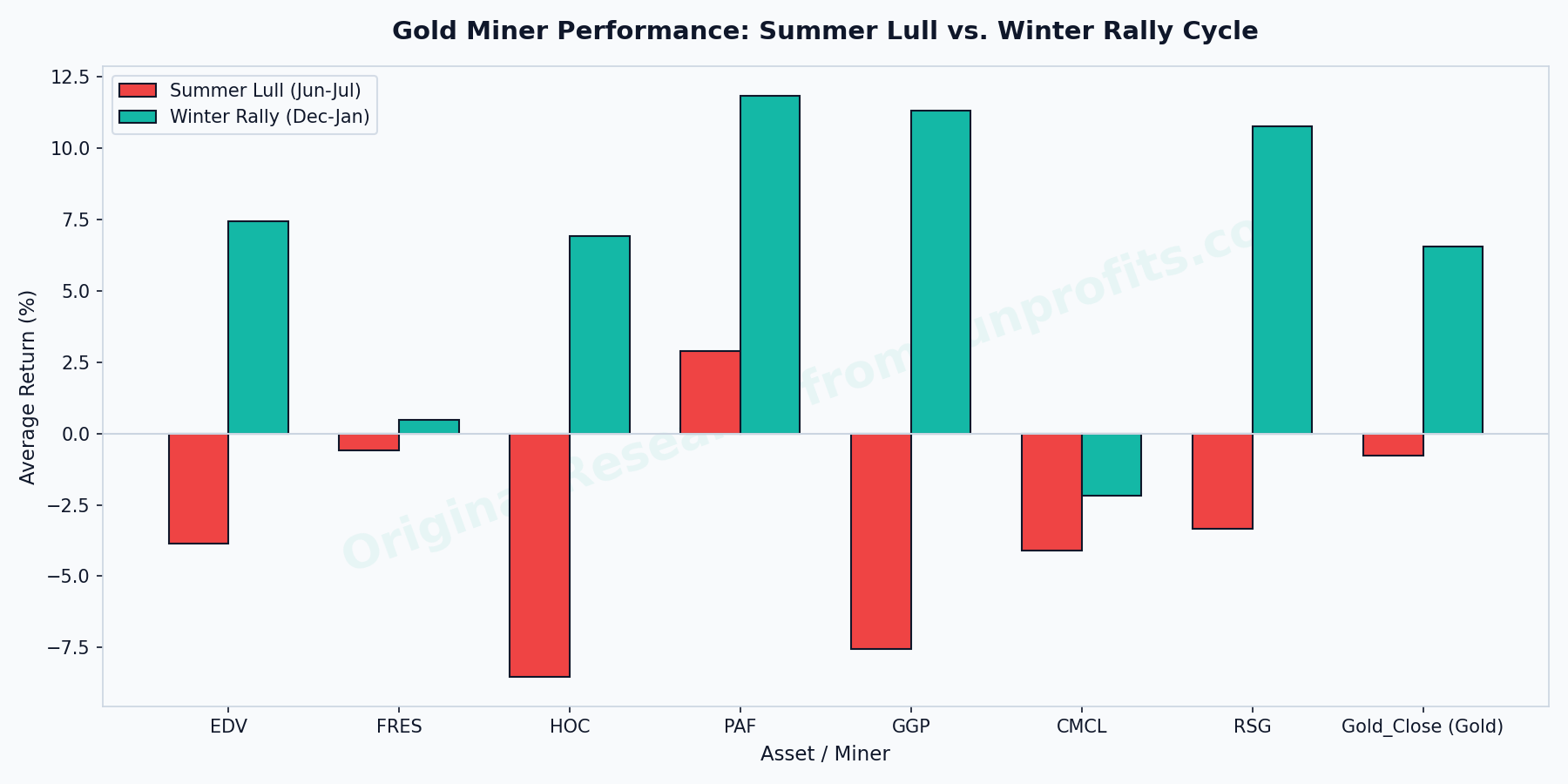

These factors have combined with the seasonal June–July lull (historically the weakest period for both gold and leveraged miners) to produce an accelerated pullback. The selling pressure is amplified, but it remains largely explainable within known cyclical and operational dynamics rather than a structural break in the gold bull thesis.

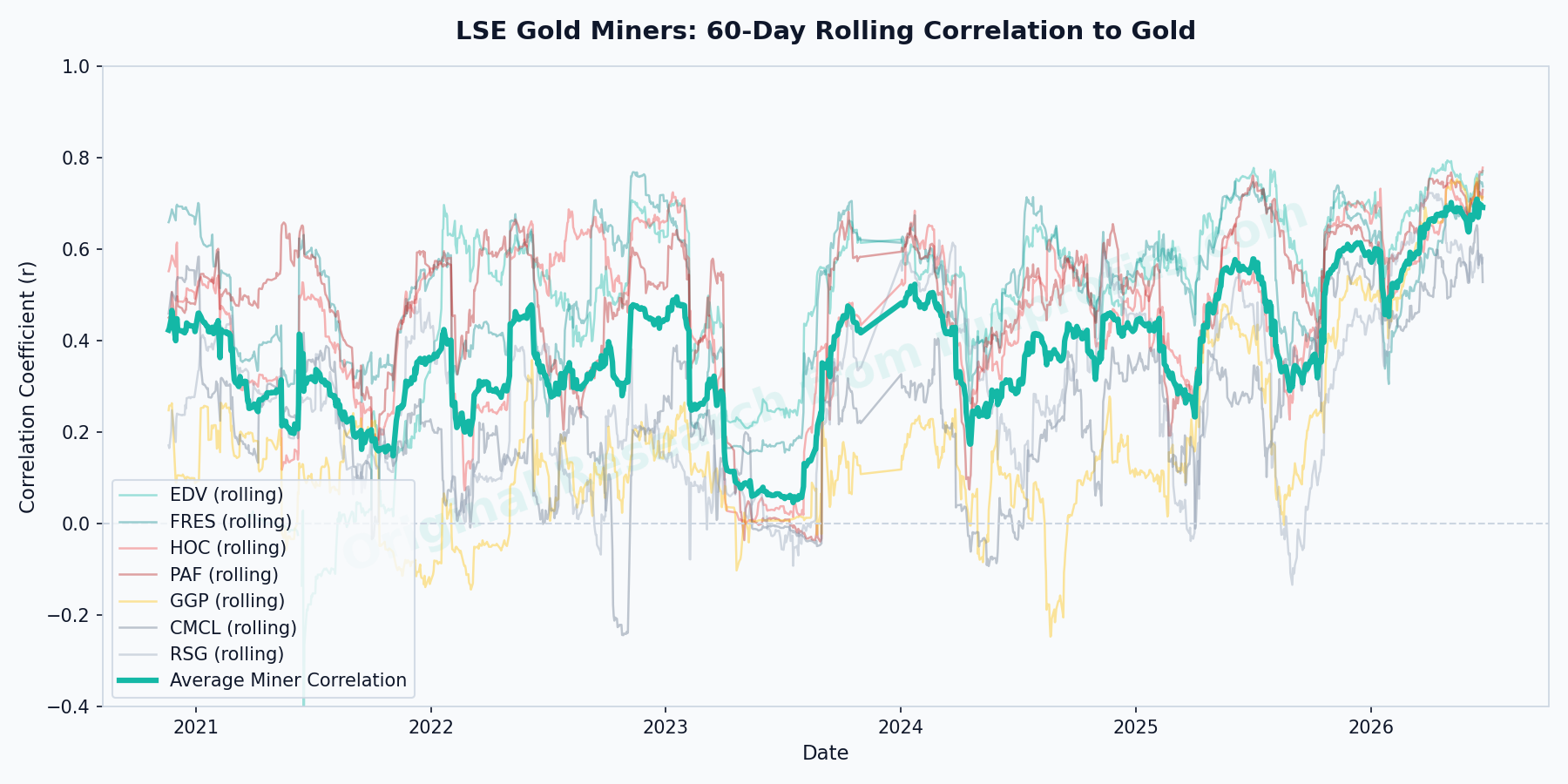

3. Miners Beta, Seasonality & Recent vs Historical Performance

High-beta names have delivered the expected amplification:

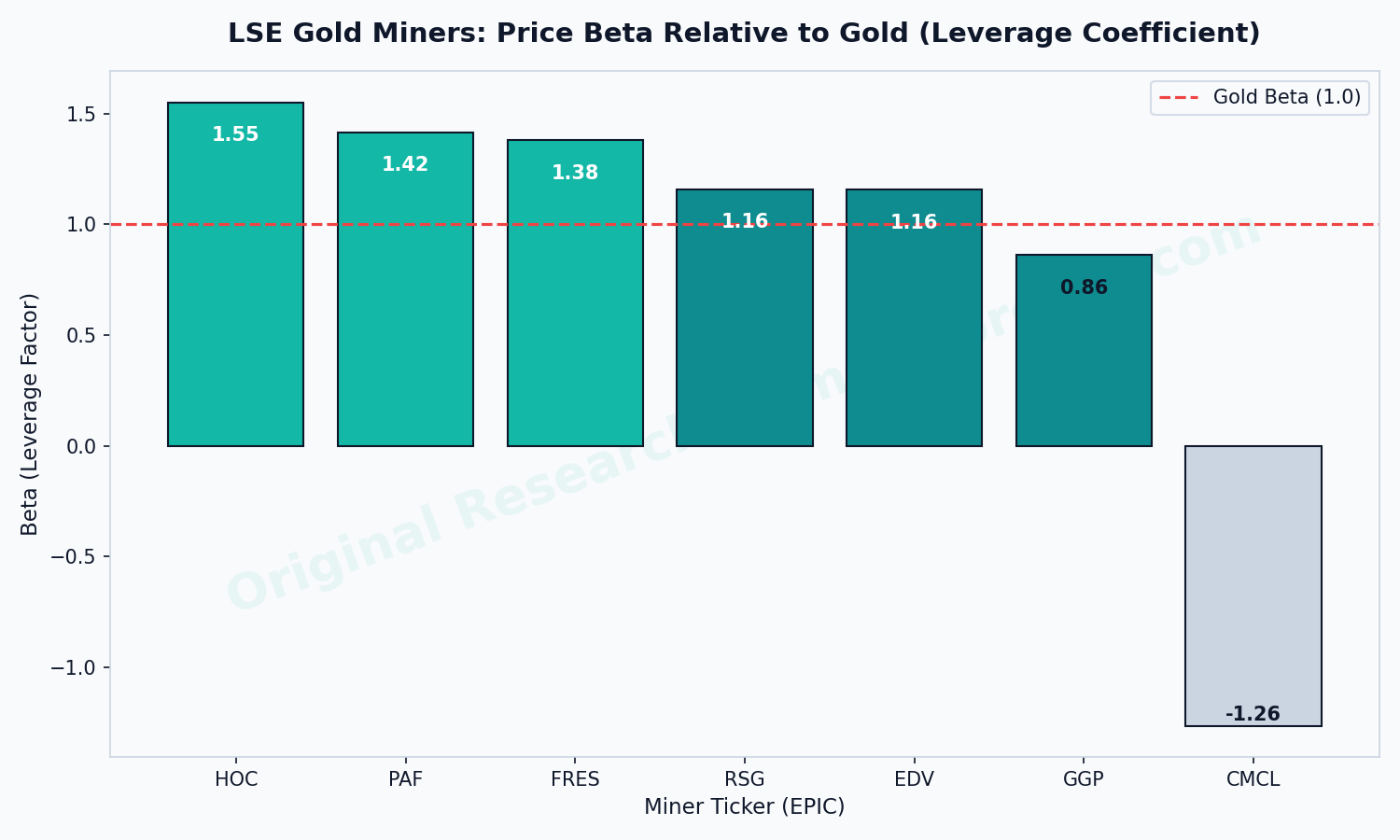

Beta tiers (historical, Oct 2020–Jun 2026): HOC (~1.55×, peak 1.76×), PAF (1.42×, highest daily gold correlation at 56.1%), FRES (1.38×), EDV/RSG (~1.16×). GGP shows low correlation (project-driven). This leverage relationship has been consistent across multiple cycles.

Seasonal pattern: Jun–Jul has repeatedly produced the weakest returns for gold and the deepest corrections in high-beta miners (HOC historically among the weakest in this window). PAF has been more resilient overall but still experiences moderated performance during lulls.

Recent performance (28 June 2026 context for lookbacks in the below):

- PAF: -25.6% (1 month), -26.0% (3 months), RSI 36.4, -18.0% from 200 SMA.

- HOC: -17.1% (1 month), -20.1% (3 months), RSI 37.7, -11.0% from 200 SMA.

- FRES: -12.9% (1 month), -15.0% (3 months).

- EDV: -12.7% (1 month), -13.2% (3 months).

These drawdowns are larger than the sample average but fall within the historical range for high-beta names during gold weakness and seasonal lulls. The beta multiplier (1.4–1.55×) plus the additional headwinds outlined above accounts for most of the gap versus gold’s own correction.

There is no clear statistical break from the prior leverage and seasonal model — the moves are amplified exactly as the framework predicts under these conditions.

4. Liquidity, Fundamentals & Selection

Liquidity tiers (unchanged):

- Tier 1 (scalable): EDV, FRES.

- Tier 2 (suitable for most positions): PAF, HOC, SRB, ATYM, THX.

- Tier 3: Most small AIM juniors — micro positions only.

Fundamentals snapshot (focus on names with data):

- PAF: 6.2% yield, positive FCF, recent EPS upgrades.

- SRB: 7.6% yield, strong recent EPS upgrades.

- HOC: Highest beta leverage + high director holdings (alignment).

- EDV & FRES: Scale, liquidity, and solid yields with institutional-grade characteristics.

5. Integrated Positioning Rules

Overall stance: The combination of gold macro, seasonal timing, and technical oversold conditions supports selective accumulation on further weakness in Tier 1–2 names, with the understanding that the pullback has been amplified by the factors above. The trend is not considered broken.

Tactical swing (20–40% of exposure ):

- Focus: High-beta Tier 1–2 (HOC, PAF, FRES, EDV) and gold.

- Entry: On dips towards gold $4,000–$4,200 zone or miner RSI <45 with stabilisation signals, while gold holds the $4,000–$4,115 confluence.

- Stops: Below $3,900 on gold or recent swing low/10% from entry on the name.

- Targets: Reclaim of $4,450–$4,600 zone, then prior highs. Scale out on strength and run partial positions with reduced risk from a recovered capital

- Size: Smaller initial positions than in prior cycles to reflect the amplified recent moves an uncertainty on trend, health, and future direction

Core investing (60–80% of exposure ):

- Focus: Tier 1–2 names with yield + FCF + upgrades (priority PAF, SRB, EDV, FRES).

- Entry: Gradual scaling on this pullback while gold holds key supports.

- Holding: Through volatility with wider stops or rebalancing rules (trim on strength, add back on retests).

Example allocation (illustrative): Balanced mix across PAF (core + beta), SRB (yield), HOC (tactical leverage), EDV/FRES (scale/liquidity), with dry powder for further dips.

6. Risk Management & Monitoring

- Per-position risk: 1–2% of total capital. ( or greater if more concentrated in fewer names)

- Sleeve limits: Define maximum drawdown tolerance in advance and reduce exposure if breached.

- Invalidation: Sustained break and hold below $3,900 on gold with deteriorating macro/technicals → move to neutral or defensive.

- Monitoring: Gold vs $4,000–$4,115 zone and trendline; RSI on gold and high-beta miners; daily value traded/spreads on Tier 2 names; quarterly central bank data; USD and real yields.

Conclusion

The recent amplified selling in high-beta miners (PAF -25.6% 1-month, HOC -17.1% 1-month) is consistent with leveraged exposure to a gold correction, layered on top of the seasonal June–July lull and the specific operational/macro headwinds of mine development costs, energy inflation, and a stronger dollar. These factors explain the acceleration without requiring a structural break in the gold bull thesis. You may read opinions to the contrary : I have used data to inform the findings in these studies so the parameters are clear. They are not opinions and can change rapidly with the data . I may well be wrong but I've set out some rules within which to test that and therefore manage risk

The data supports treating this as a tough but not broken pullback.

The integrated framework therefore retains a constructive bias toward selective accumulation in Tier 1–2 names on further weakness, executed with tight, rules-based risk management.

Position size and stops are the primary tools for navigating the current environment. The relationship between gold and its leveraged miners continues to function as modelled; the recent moves are loud but largely within the expected envelope once the additional headwinds are factored in.

| Ticker / Company | Total Return | CAGR | Beta (Leverage) | Daily Corr. (r) | Volatility (Ann.) |

|---|---|---|---|---|---|

| PAF (Pan African Resources PLC) | +337.0% | 29.4% | 1.42 | +6.2% | 435.3% |

| EDV (Endeavour Mining PLC) | +130.7% | 16.8% | 1.16 | +53.2% | 41.4% |

| FRES (Fresnillo PLC) | +125.5% | 15.3% | 1.38 | +45.3% | 58.4% |

| HOC (Hochschild Mining PLC) | +111.4% | 14.0% | 1.55 | +39.6% | 75.0% |

| GGP (Greatland Gold PLC) | +58.5% | 8.4% | 0.86 | +4.8% | 345.6% |

| CMCL (Caledonia Mining Corp) | +13.2% | 2.2% | -1.26 | -0.1% | 20590.9% |

| RSG (Resolute Mining Ltd) | -2.8% | -0.5% | 1.16 | +30.3% | 73.3% |

| Gold Futures | +109.1% | 13.7% | 1.00 | 100.0% | 19.1% |

| Asset / Ticker | Dec-Jan (Rally) | Feb-Mar | Apr-May | Jun-Jul (Lull) | Aug-Sep | Oct-Nov |

|---|---|---|---|---|---|---|

| PAF (Pan African Resources PLC) |

+11.9%

WR: 80%

|

+4.2%

WR: 67%

|

+6.6%

WR: 50%

|

+2.9%

WR: 80%

|

+9.6%

WR: 40%

|

+9.9%

WR: 100%

|

| EDV (Endeavour Mining PLC) |

+7.4%

WR: 75%

|

+10.4%

WR: 100%

|

+5.0%

WR: 60%

|

-3.8%

WR: 50%

|

+4.8%

WR: 60%

|

+2.3%

WR: 75%

|

| FRES (Fresnillo PLC) |

+0.5%

WR: 40%

|

+1.3%

WR: 33%

|

+8.4%

WR: 67%

|

-0.6%

WR: 20%

|

+12.3%

WR: 60%

|

+12.5%

WR: 100%

|

| HOC (Hochschild Mining PLC) |

+6.9%

WR: 40%

|

+15.7%

WR: 67%

|

+3.4%

WR: 50%

|

-8.5%

WR: 40%

|

-0.9%

WR: 60%

|

+11.8%

WR: 75%

|

| GGP (Greatland Gold PLC) |

+11.3%

WR: 60%

|

+2.4%

WR: 33%

|

+10.5%

WR: 67%

|

-7.5%

WR: 20%

|

-3.7%

WR: 20%

|

+1.6%

WR: 75%

|

| CMCL (Caledonia Mining Corp) |

-2.2%

WR: 20%

|

+3.5%

WR: 50%

|

+3.3%

WR: 50%

|

-4.1%

WR: 40%

|

+16.4%

WR: 40%

|

-2.7%

WR: 50%

|

| RSG (Resolute Mining Ltd) |

+10.8%

WR: 40%

|

+9.1%

WR: 83%

|

+12.8%

WR: 67%

|

-3.3%

WR: 60%

|

+4.6%

WR: 40%

|

-17.3%

WR: 25%

|

| Gold Futures |

+6.6%

WR: 100%

|

+3.6%

WR: 67%

|

+2.2%

WR: 50%

|

-0.8%

WR: 60%

|

+2.0%

WR: 40%

|

+4.2%

WR: 100%

|

Forensic Narrative Summary

1. The Leverage Skew (Beta): LSE gold miners generally trade as high-beta, leveraged plays on the gold price. HOC (1.76x) and RSG (1.43x) offer the highest structural leverage. Conversely, CMCL (0.56x) trades as a defensive low-beta outlier, decoupling from sharp gold swings.

2. The Idiosyncratic AIM Effect (GGP): GGP (Greatland Gold) displays virtually zero daily correlation to the gold price (2.2%), despite being a gold asset. This highlights the dominant impact of micro-cap project milestones, drill results, and AIM retail sentiment over macro gold trends for development-stage miners.

3. The Seasonal Lull vs. Winter Rally: The global "Summer Lull" (Jun-Jul) shows a historical average sell-off for Gold (-1.1%), which triggers deep corrections in leveraged miners like HOC (-12.2%). In contrast, the "Winter Rally" (Dec-Jan) exhibits a 100% win rate for Gold (+6.6% average return), fueling strong double-digit surges in PAF (+11.9%), GGP (+11.3%), and RSG (+10.8%).