Markets yo-yo back with a bullish bent as the NMX reverses many of yesterday’s sudden and dramatic losses. This level of skittishness is often evident when markets are struggling to find direction following several weeks of consolidation. Today’s rally of 0.8% in the NMX with participation by much of the MCIX and supported by over 1% gains in tech suggest that the bullish bias is winning. We would expect the overall market to rally from here unless trade tariffs rhetoric worsens.

Sectors outperforming today included Software (+2.7%) driven mainly by a 10% rise in CCC, Pharm (INDV +8%, AZN +3.5%), while Media T&L, A&D , Tobacco and Bevs all outperforming the index and rising more than 1%.

Oil sank over 1% following yesterday’s almost 6% drop which depressed O&G while metals continues to languish with copper losing over 1%: this weighed on Mining. The resource sectors have tended to be a barometer of trade tensions with mining companies reacting dramatically to increased threats. Oil may well have double topped on the $80 this may depress oilers if continued weakness is seen. Dr Copper is not yet signalling and end to the recent softness. A rally in copper would support the bullish sentiment

What a difference a day can make, trade war escalations now look set to get beyond sabre rattling to much more damaging levels as Trump threatens hundreds of billions of goods in line for tariffs from China while simultaneously alienating Germany as “under Russian control”. The inherent stability of one individual seems to have echoed in global markets with European and UK markets ending heavily in the red. The NMX and UKX sank by over 1.2% owing mainly to heavy losses in Mining (-3.6%) , O&G (-2.5%) with losses across most sectors.

The dramatic nature of today’s losses may well call into question the nascent summer rally: price action over the next few days will clarify

Some stand-out losses on the day include INDV down almost 35% and MCRO down almost 10% on the day.

AIM fared best on the day off only 0.5%. TechMARK was off over 1.2%

Oil tumbled almost 3% while GBP was flat on the day .

Copper is staging a relief rally which may well auger well for overall market health. However the huge sways in commodities are direct echoes of trade tensions and their global impact

Flat day for the major indices with little or no change in NMX, UKX and MCIX. AIM and TechMARK continued to advance up almost 0.5% in each case. O&G services continues to outperform all sectors as the continued strength in oil augers well for exploration and production and therefore Oil Services companies.

Software also advance led higher by Softcat while the larger , O&G and Pharm sectors did most of the heavy lifting to offset losses in other sectors There were significant losses for Utilities (-2%) , Telecomms (-2%) though the biggest dents to the day;s rise came from Mining (-1%) , Banks and Financial Services

Oil continues to rally but pulled back from the day’s highs

Metals continue to be flat although copper has gained slightly. The increased trade tariffs tensions have weighed heavily on commodities

GBP rallied somewhat on improving GDP data adding to recent strong PMIs although political uncertainty over Brexit is hampering any significant rally

The decisive move in the NMX forms a break-out from the sideways consolidation over the past month and and a half although volume is still below normal. This suggest we should rally over the summer and potentially form new highs

<a href=”http://79.170.40.181/runprofits.com/?page_id=4414″ target=”_blank” rel=”noopener”>Strong bounce in the NMX which sold-off into the close but remained up 0.55% on the day. The lead sectors were Fixed Line Comms (+2.6%), Tobacco (+2.2%) with Mobile, Life Ins, Pharm all up over 1%</a>

MCRO sold-off -8% to take Software down over 2% on the day : while Mining (-1.8%) was affected by GLEN drop of over -8% on US fraud investigations

The MCIX was up a modest 0.3% while AIM gained 0.44% but remains short term bearish

The TechMARK gained over 0.5% and is currently the most bullish index in the UK mirroring the role of technology in the US which may well be bullish the overall market

GBP gained against the dollar while Oil sold-off over 0.6% but remains bullish across all timescale

Volumes may be light next week as many US trading desk will take holidays for 4th July

<a href=”http://79.170.40.181/runprofits.com/?page_id=4411″ target=”_blank” rel=”noopener”>Sectors and Shares Update</a>

<a href=”http://79.170.40.181/runprofits.com/?page_id=4406″ target=”_blank” rel=”noopener”>Short Interest Update</a>

All of the UK markets sank heavily today as trade tensions mount and the Brexit blues start to bite. The major indices were down over 1% led in the main by Mining down over 3% while T&L, Banks, Pharm and O&G were all down over 1%. Utilities did catch a bid perhaps in a flight to defensive

Both AIM and the TechMARK suffered to a lesser degree off around 0.8% though these often lag the main markets so if selling is extended expect these to follow the main markets

NMX, UKX and MCIX are all considerably below their 8,21 and 50 MAs signalling a trend change and more selling to come

AIM is finding support at its 50DMA which it may well check again tomorrow

Oil fell almost 2% while GBP weakened further against USD while USD/JPY looks set for break-out signalling a flight to safety.

Gold has continued to sell and should find support around 1240 as a double bottom with the Dec 17 lows

Given the level of selling especially in the US, some relief may be found soon with a potential catalyst being another Trumpian capitulation or Twitter flurry. That said, tomorrow is the last trading day before the US holidays

Volumes may be light next week as many US trading desk will take holidays for 4th July

<a href=”http://79.170.40.181/runprofits.com/?page_id=4337″ target=”_blank” rel=”noopener”>Sectors and Shares Update</a>

<a href=”http://79.170.40.181/runprofits.com/?page_id=4325″ target=”_blank” rel=”noopener”>Short Interest Update</a>

NMX rallied almost 1% from a boost in oil prices up 1.6% and a weaker pound.

Sectors doing the heavy lifting were O&G (+3%), Mining (+1.5%) , T&L (+1.3%)with almost all sectors in the green on the day except Gen Retail , REITS and Food Producers. The bouncehelped the NMX recapture the 50DMA but by a thread: the mid term bias is still downward although volumes are light. European markets have all turned bearish joining the HSI.

The MCIX was up a modest 0.4% not receiving the boost from the big resource sectors while AIM was flat on the day

The TechMARK staged a brief recovery rally and recaptured it 50DMA but remains sluggish and looks set to sell-off further

Beverages (+0.7) and utilities (+0.5%)

The drag on the index came from weakness in mining, insurance and financial services. However, GBP continues to weaken and oil price are rallying which should lift the UKX and NMX

The MCIX closed down -0.8 with AIM down almost 1% and the TechMARK continuing to

falter

All of the UK indices not sit below their 2, 21 and 50 day moving averages in anextended pullback

The outperforming sectors continue to be O&G (including services), A&D and Tobacco

<a href=”http://79.170.40.181/runprofits.com/?page_id=4288″ rel=”noopener” target=”_blank”>NMX rallied over 0.6% before selling-off slightly closing up 0.3% on the day.

The bounce was led in the main by O&G (+1.2%), Mining(+1%) and Construction (+1%) The main indices do remain short to mid term bearish with aloss of momentum and lower average volume suggesting more downside is likely from here.The MCIX sold off yesterday closing down 0.12 while AIM rallied only 0.1%.

The MCIX has joined both the NMX and UKX in losing its 50DMA and turning more bearish.

TechMARK was flat on the day while Oil rallied which helped lift both the NMX and UKX.

Many of the more significant sectors remain in bearish territory and include Banks, O&G, Pharm, Tobacco and Life Insurance.

In Europe the DAX, Euronext 100 and CAC are all bearish across all major timescales while in Asia the HIS is similar with the NIK bearish across short and mid-term timescales.

Clearly the US led trade wars are having an impact combined with seasonal weakness and some profit taking.

All of the metals are bearish while Oil is bearish on the short to medium term but retains its 100 and 200 DMAs for now.</a>

<a href=”http://79.170.40.181/runprofits.com/?page_id=4285″ target=”_blank” rel=”noopener”>Sectors and Shares Update</a>

<a href=”http://79.170.40.181/runprofits.com/?page_id=4269″ target=”_blank” rel=”noopener”>Short Interest Update</a>

Mining (-3.8%), O&G(-3.1%) , Construction (-2.8%) with only 2 sectors flat or in the green

While much of the narrative is attributed to Trump’s aggressive trade manoeuvres, we are almost at the end of June and second quarter rebalancing and profit taking. A June Swoon is therefore not unexpected and should be a healthy pullback

The most bullish sector over the past week and month have been Food and Drug retail, Fixed Line Comms, Food Producers and Media with Tobacco making a resurgence of later

The most bearish include, Life Insurance, Construction, Banks, Mining

While the bigger more resource intensive indices were hit hardest today, the MCIX was down 1.14%, AIM (-1%),

TechMARK (-1.7%)

GBP was flat against USD while oil sold-off over 1.6% wit the metals similarly negative on the day

At the time of writing the S&P is down almost 2% on high volumes with the NASDAQ off almost 3% , meanwhile

the VIX has spiked almost 20% to 17

The MCIX fared better closing up 0.5% while AIM gained 0.6% and the TechMARK a similar 0.5%

Sectors leading the rally were Telecoms (+2.7%), Tobacco (+2.6%), Media (+1.2%) while the laggards included o&G (-0.9%), Gen Retail (-0.4%)

Brent lost 0.9% and is short and medium term bearish having tried and failed to regain the 50DMA

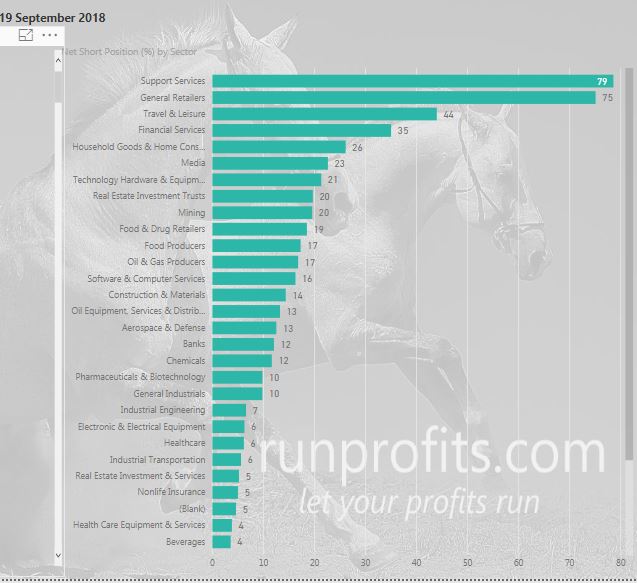

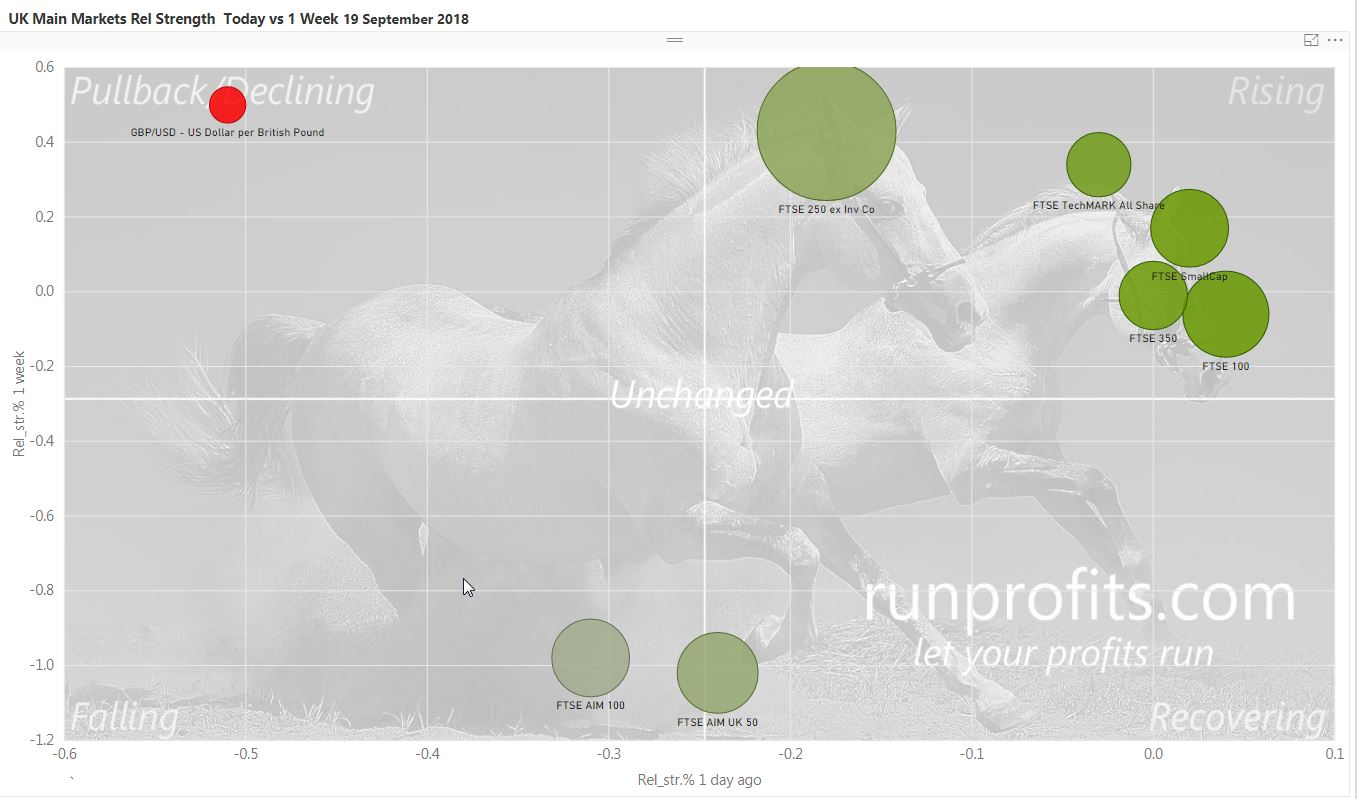

UK Markets Narrative Wed 19 Sep 18 EOD

Overall the price action in the major indices was relatively muted with the NMX and UKX rallying 0.4%, : MCIX up 0.25% with AIM flat and the TechMARK up 0.4%. Oil rallied 0.4% to close just short of the $80 mark.

Of the three major indices, the MCIX is the only one above its 21 EMA while the UKX and NMX are still relatively sideways: this may well be a basing consolidation before a move higher but caution is still advised in trading long until more clarity on direction is apparent.

GBP closed flat on USD for the day, copper was flat while gold and silver rallied 0.5% and 0.9% respectively.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Tues 18 Sep 18 EOD

The announced takeover of JLT boosted Non-Life insurance up almost 2.5% while industrial metals shone brightest close up 3%

In underperformers, Tobacco once again lagged behind down 1.9% while Media and Forestry lost almost 1%

Of the major UK indices, NMX and UKX closed flat, MCIX up 0.4%, AIM down -0.7% and TechMark unchanged.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Mon 17 Sep 18 EOD

Both the NMX and UKX were almost unchanged on the close with the MIC marginally positive by less that 0.1%. AIM did almost nothing while the TechMARK was totally unchanged

In sectors, Utilities, tech Hardware Comms and O&G Services all advanced by 1% or more while Beverages , Software and Life Insurance all retreated by almost 1%.

In AIM, the roller coaster nature of junior oilers was illustrated by CLON’s 170% bump while PET jumped 62%in a day while PAF lost 17%

Oil closed down by 0.2% while copper gained o.3% along with most of the base metals which rallied gold (+0.75%) and silver (+1%) also caught a bid although neither have been able to sustain a rally all summer. If continued USD weakness persists then these metals may yet shine

Of interest is that UKX remained flat even as GBP advanced over 0.6% against USD: this is potentially on the back of more optimism on Brexit which may unwind the inverse correlation between the UK mega stocks and USD. i.e bullishness on a good Brexit outlook outweighs the negative drag of a stronger pound. Time and price action will tell if this hypothesis has any veracity

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Thurs 13 Sep 18 EOD

The poorest performing sectors of note were Tobacco (-2%), Gen Retail and Media both -1.3%, Personal goods (-1.2%) while Pharm, A&D and O&G all underperformed the main index

AIM was relatively flat down -0.13% while the TechMARK also outperformed the main indices down only 0.35%

Oil also gave back 1.4% today although copper continued to rally.

The weakness in USD has given cheer to the US equity markets, this may translate to the UK and Europe tomorrow but for now the outlook remains muted for the main indices all of which remain below their 8,21, 50, 100 and 200 day moving averages. More green shoots are needed before taking anything other than strongly outperforming longs on an RSI basis

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Fri 07 Sep 18 EOD

Mining (-1.7%) is yet again the underperforming sector which seems to be signalling more systemic global effects are in play. This is amplified by the developing markets economies crises: all are casualties of both a strong dollar and reduced liquidity as monetary policy across the globe adjusts and tightens.

Banks were also off almost 1.2% while O&G closed down 0.9%

The TechMARK managed to close the day in the green up 0.3%, the only UK index to close up.

Of the few green shoots in today’s sea of red were Mobile (+0.7%) ,A&D (+0.5%), Health Care Equip (+2.2%) with Software up over 1%

Oil closed down on the day by 0.7%, GBP up and the metals mixed: copper up 0.3% but gold down reflecting the stronger dollar. Silver rallied by 0.7% which, combined with a partial recovery in copper and iron ore, may be early signals that the worst is over for the miners. This is in turn would be bullish for the UKX and help shift market sentiment which is currently maudlin

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Tues 11 Sep 18 EOD

Other notable sectors that caught a bid today included Services, Personal Goods and Pharm all ending the day in the green.

However, Banks, T&L, Tobacco and Media all joined Mining in closing firmly in the red today

Chart patterns across the UKX, NMX and MCIX all signal a reversal is now due so a rally is to be expected in the next few days from fairly oversold conditions.

AIM closed down -0.3% while the TechMARK ended the day in the green up o.2%

GBP continues to hover around the $1.30 level which has proven to be a magic number over the past few months. With today’s unemployment figures combined it wage increase and a firmer GDP from yesterday, the path for another rate rise does seem set for later in 2018. That combined with more dovish rhetoric for the EU on Brexit would suggest that GBP is set to rally further

In other commodities, copper is down on the day as is iron ore and all the base metals. Neither gold nor silver can seem to catch a sustainable bid in the face of the strong dollar and trade tensions. Unless these conditions change, the mining sector remains too uncertain on any trading horizon until more clarity on macro conditions is available.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Wed 05 Sep 18 EOD

AIM has finally taken a breather from its relentless upward climb closing down 0.6%. The TechMARK also closed down almost 1% and testing its 200MA before bouncing into the close.

Of the Top 10 sectors, Banks, Mining, Tobacco and Life Insurance are below all of their short medium and long-term MAs including their 200MAs with Mining and Tobacco almost 10%b below their 200MA

While some relief in the selling may be on the cards, the overall timbre of the markets has turned bearish

Pharmaceuticals and Support Services remain the most resilient sectors in the top 10 while Non Life Insurance, O&G Services, Auto Parts and leisure Goods remain the most bullish

GBP reversed sharply on USD today on news that Germany may be more open to a Brexit deal. Brent crude closed down almost 1% on the day which added to the UKX woes while metals were mixed with iron ore and copper rallying modestly

UK Markets Close Mon 03 Sep 18

The UKX was also boosted by a rise in oil prices with Brent up 0.6% at pixel time. The NMX followed suit with the UKX closing up 0.8%. Both these indices recapture their 200MAs which is a positive result though they are firmly below their 100 and 50 MAs and their 21 and 8 EMAs so caution should be taken. That the 200MA has been recaptured may be significant although volumes were light. Confirmation of any rally would be needed in the next few days with prices closing above the 21EMA ideally on two consecutive days.

The MCIX by contrast remain better behaved following the 8 EMA and closing flat on the day unmoved by GBPs episodic spasms. AIM rallied 0.3% keeping tis upward trajectory though forming a doji on the day which may be signalling a pause in its rally

The TechMARK had a strong day up 0.9% buoyed in the main by SN, MCRO and a rebound in SGE

Today’s leading sectors of size were O&G up 1.7%, Mobile (+1.2%), Health Care Equip (+1.2%), Life Insurance (+1.5)

Underperforming sectors included REITS (-0.7%), F&D Retail (-0.2%) and Utilities (-0.2%)

GBP down 0.8% on USD and EUR. Gold flat, Silver down 0.3%, copper down 1.5%

Welcome to runprofits.com

Site is available to test users . You can register to use the site for free. Help and how to guides available by October 18.

Financial Week Ahead 17-23 Sep 2018

Companies Reporting

Over 60 companies reporting this week, most of them AImers

FTSE 100 - BAB, KGF and SMIN

FTSE 250 - DCG, OCDO, SGC, KIE

AIM All - 39 including CAML, QXT, SFE, CALL, EYE, FST, BGO, KWS

Economic Announcements

Wed - UK CPI, PPI, RPI Inflation figures

Thurs - Retail Sales UK

Fri - UK public sector borrowing

Full details for each day and weekly, monthly overview in Calendar Events

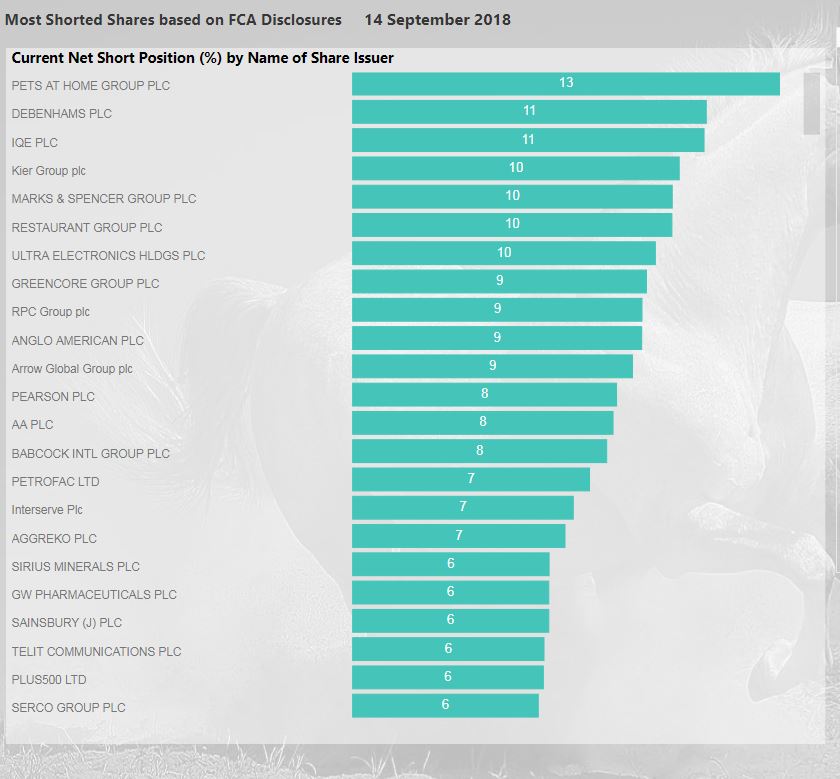

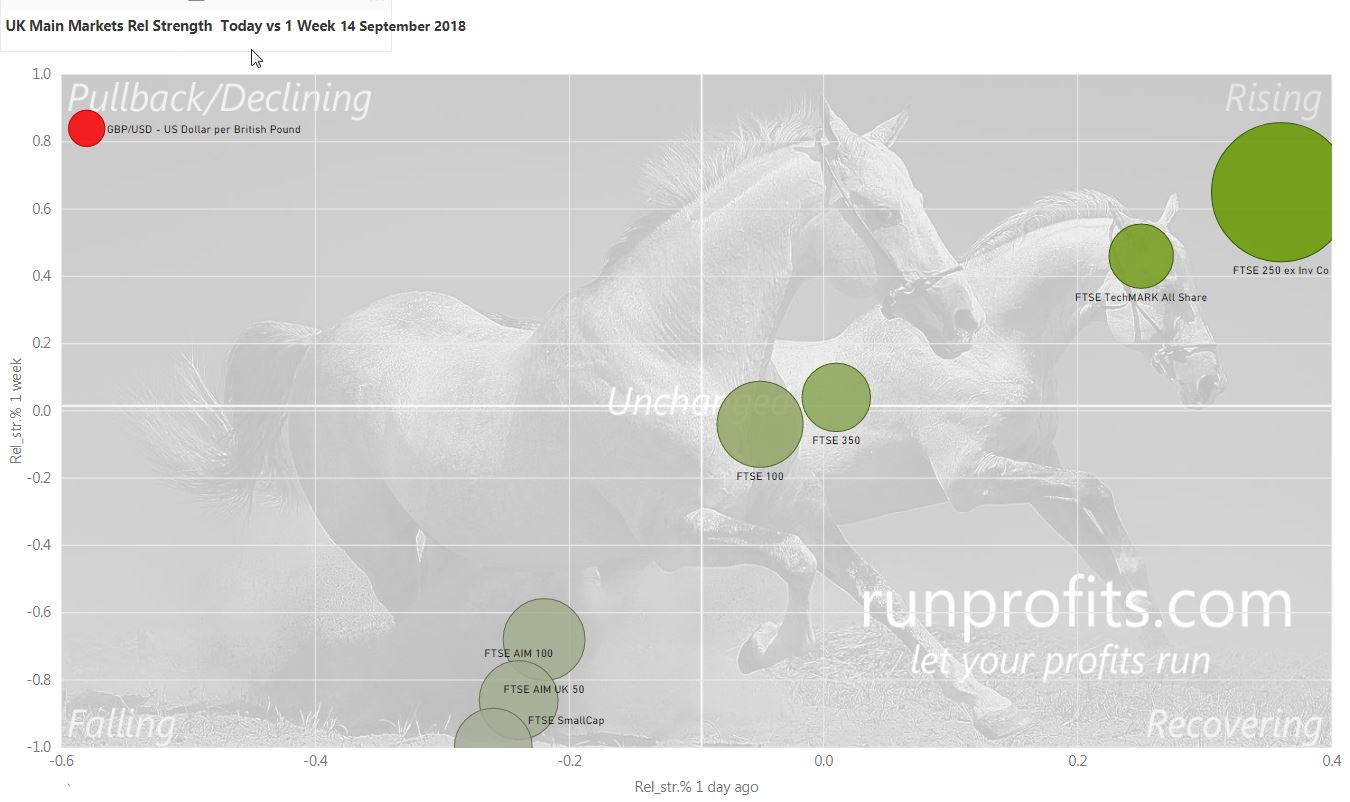

UK Markets Narrative Fri 14 Sep 18 EOD

Outperforming sectors included A&D (+2.2%), Construction (+1.8%), FS (+3.8%) and Mining up 1%

Utilities and electricity continued to underperformed with SSE losing another 3%. Tobacco closed down again by 0.7%

AIM was flat while the TechMARK closed up 0.6% driven in the main by the Pharmas rallying especially OXB

Oil has pulled back significantly from its recent touch on $80 owing to dissipating fears of the severity of Florence and it impact on US oil producers.

In the metals, copper took a break from its recent streak to close down 1% while iron ore gained almost 0.8%. Both gold and silver were down on the day as inflation fears seem muted

GBP touched $1.31 today before pulling back to close down almost 0.25%

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Wed 12 Sep 18 EOD

Today’s standout sector was Tobacco rallying almost 6% from a very oversold position (close to a bear correction of almost 20%). Mining came bouncing back rising 2.3% cheered by a sharp rebound in copper, zinc and many of the base metals rising over 2% on the day

An early rally in oil also lifted the O&G sector while T&L and Pharm also participated in today’s rally

Banks have continued to sell-off closing down 0.3% on the day while Insurance, Media and Utilities were all in the red with SSE falling over 8% on a profit warning

Oil closed up 0.4%, copper up over 2.5% and GBP flat against USD at $1.30

Despite today's rally all of the major indices remain bearish and below all moving averages with the exception of AIM which still above is 100 and 200 MAs.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Mon 10 Sep 18 EOD

Bullish comments from Barnier on Brexit helped to boost GBP which rallied above the significant $1.30 level: this also marks a close above the 50MA for the first time since April 2018. If this holds over the next few days then the worst could be over for sterling for now which will put pressure on the FTSE 100

While the UKX and NMX closed flat on the day, the MCIX rallied 0.4% while AIM closed down 0.2% and the TechMARK flat on the day

None of the price action today changes the overall bearish tone of the markets: the lack of any relief rally today may well be ominous and a preface to more selling to come

Today’s outperforming sectors of significance were Household and Home construction (+0.8%), Media (+0.5%) and Personal Goods (0.4%)

Mining continues to sell-off down 0.65% today and over 11% in the past month: , Tobacco lost an additional 0.7%

Looking across the sectors shows a sea of red across all timescales with most sectors having dropped below their 200MAs: only Pharm, Media and Support Services are clinging to their 200MA in the top 10 sectors

Failing a significant rally in the next couple of days, the most likely direction of travels seems to be downward with a bias to the short side

Brent rallied 0.5% on the day with the metals mostly flat on the day

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Thurs 06 Sep 18 EOD

Today’s selling was a continuation of the bearish sentiment evident across the UK and European major indices. The UKX closed the day down 0.9% and close to its lows on the day while the NMX sold-off by 0.8%. The MCIX fared marginally better at 0.6% while AIM bucked the trend rallying 0.35% aided by the likes of FDEV rallying 14% while HZD gained 8% and TAP 6%

The TechAMRK lost over 0.8% with the biggest loser being GNS down almost 7% with SPT and MCGN down 3%

In terms of sectors, the biggest loser were Mining (-2.3%), O&G (-1.5%) and Pharm (-1.5%) and Banks (-1.3%)

Defensive sectors all posted gains including Utilities (+1.8%), Comms (+0.7%) and Construction (+0.7%)

Brent reversed heavily during the day from posting a pop by 0.3% to closing the day down almost 1.5%

GBP rallied against USD gaining 0.2% and approaching the $1.30 level

Neither the fall in oil nor the rally in GBP can offset the wholesale selling across the major indices. September is often a poor month for equities as traders return from holidays.

UK Markets Close Tues 04 Sep 18

With only Banks, Electricity and Beverages moderately in the green: the UKX and NMX ended the day down over 0.6% reversing much of yesterday’s gains and closing below the 200Mas again

The TechMARK closed down almost 0.9% with SGE down 2%, AZN -1.8%, AVV -1.9%

AIM closed moderately in the green while Brent continued to rally up 0.4%.

GBP closed down over 0.4% against USD but this failed to boost the major indices

UK Markets Narrative Wed 19 Sep 18 EOD

Overall the price action in the major indices was relatively muted with the NMX and UKX rallying 0.4%, : MCIX up 0.25% with AIM flat and the TechMARK up 0.4%. Oil rallied 0.4% to close just short of the $80 mark.

Of the three major indices, the MCIX is the only one above its 21 EMA while the UKX and NMX are still relatively sideways: this may well be a basing consolidation before a move higher but caution is still advised in trading long until more clarity on direction is apparent.

GBP closed flat on USD for the day, copper was flat while gold and silver rallied 0.5% and 0.9% respectively.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Tues 18 Sep 18 EOD

The announced takeover of JLT boosted Non-Life insurance up almost 2.5% while industrial metals shone brightest close up 3%

In underperformers, Tobacco once again lagged behind down 1.9% while Media and Forestry lost almost 1%

Of the major UK indices, NMX and UKX closed flat, MCIX up 0.4%, AIM down -0.7% and TechMark unchanged.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Mon 17 Sep 18 EOD

Both the NMX and UKX were almost unchanged on the close with the MIC marginally positive by less that 0.1%. AIM did almost nothing while the TechMARK was totally unchanged

In sectors, Utilities, tech Hardware Comms and O&G Services all advanced by 1% or more while Beverages , Software and Life Insurance all retreated by almost 1%.

In AIM, the roller coaster nature of junior oilers was illustrated by CLON’s 170% bump while PET jumped 62%in a day while PAF lost 17%

Oil closed down by 0.2% while copper gained o.3% along with most of the base metals which rallied gold (+0.75%) and silver (+1%) also caught a bid although neither have been able to sustain a rally all summer. If continued USD weakness persists then these metals may yet shine

Of interest is that UKX remained flat even as GBP advanced over 0.6% against USD: this is potentially on the back of more optimism on Brexit which may unwind the inverse correlation between the UK mega stocks and USD. i.e bullishness on a good Brexit outlook outweighs the negative drag of a stronger pound. Time and price action will tell if this hypothesis has any veracity

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Thurs 13 Sep 18 EOD

The poorest performing sectors of note were Tobacco (-2%), Gen Retail and Media both -1.3%, Personal goods (-1.2%) while Pharm, A&D and O&G all underperformed the main index

AIM was relatively flat down -0.13% while the TechMARK also outperformed the main indices down only 0.35%

Oil also gave back 1.4% today although copper continued to rally.

The weakness in USD has given cheer to the US equity markets, this may translate to the UK and Europe tomorrow but for now the outlook remains muted for the main indices all of which remain below their 8,21, 50, 100 and 200 day moving averages. More green shoots are needed before taking anything other than strongly outperforming longs on an RSI basis

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Fri 07 Sep 18 EOD

Mining (-1.7%) is yet again the underperforming sector which seems to be signalling more systemic global effects are in play. This is amplified by the developing markets economies crises: all are casualties of both a strong dollar and reduced liquidity as monetary policy across the globe adjusts and tightens.

Banks were also off almost 1.2% while O&G closed down 0.9%

The TechMARK managed to close the day in the green up 0.3%, the only UK index to close up.

Of the few green shoots in today’s sea of red were Mobile (+0.7%) ,A&D (+0.5%), Health Care Equip (+2.2%) with Software up over 1%

Oil closed down on the day by 0.7%, GBP up and the metals mixed: copper up 0.3% but gold down reflecting the stronger dollar. Silver rallied by 0.7% which, combined with a partial recovery in copper and iron ore, may be early signals that the worst is over for the miners. This is in turn would be bullish for the UKX and help shift market sentiment which is currently maudlin

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Tues 11 Sep 18 EOD

Other notable sectors that caught a bid today included Services, Personal Goods and Pharm all ending the day in the green.

However, Banks, T&L, Tobacco and Media all joined Mining in closing firmly in the red today

Chart patterns across the UKX, NMX and MCIX all signal a reversal is now due so a rally is to be expected in the next few days from fairly oversold conditions.

AIM closed down -0.3% while the TechMARK ended the day in the green up o.2%

GBP continues to hover around the $1.30 level which has proven to be a magic number over the past few months. With today’s unemployment figures combined it wage increase and a firmer GDP from yesterday, the path for another rate rise does seem set for later in 2018. That combined with more dovish rhetoric for the EU on Brexit would suggest that GBP is set to rally further

In other commodities, copper is down on the day as is iron ore and all the base metals. Neither gold nor silver can seem to catch a sustainable bid in the face of the strong dollar and trade tensions. Unless these conditions change, the mining sector remains too uncertain on any trading horizon until more clarity on macro conditions is available.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Wed 05 Sep 18 EOD

AIM has finally taken a breather from its relentless upward climb closing down 0.6%. The TechMARK also closed down almost 1% and testing its 200MA before bouncing into the close.

Of the Top 10 sectors, Banks, Mining, Tobacco and Life Insurance are below all of their short medium and long-term MAs including their 200MAs with Mining and Tobacco almost 10%b below their 200MA

While some relief in the selling may be on the cards, the overall timbre of the markets has turned bearish

Pharmaceuticals and Support Services remain the most resilient sectors in the top 10 while Non Life Insurance, O&G Services, Auto Parts and leisure Goods remain the most bullish

GBP reversed sharply on USD today on news that Germany may be more open to a Brexit deal. Brent crude closed down almost 1% on the day which added to the UKX woes while metals were mixed with iron ore and copper rallying modestly

UK Markets Close Mon 03 Sep 18

The UKX was also boosted by a rise in oil prices with Brent up 0.6% at pixel time. The NMX followed suit with the UKX closing up 0.8%. Both these indices recapture their 200MAs which is a positive result though they are firmly below their 100 and 50 MAs and their 21 and 8 EMAs so caution should be taken. That the 200MA has been recaptured may be significant although volumes were light. Confirmation of any rally would be needed in the next few days with prices closing above the 21EMA ideally on two consecutive days.

The MCIX by contrast remain better behaved following the 8 EMA and closing flat on the day unmoved by GBPs episodic spasms. AIM rallied 0.3% keeping tis upward trajectory though forming a doji on the day which may be signalling a pause in its rally

The TechMARK had a strong day up 0.9% buoyed in the main by SN, MCRO and a rebound in SGE

Today’s leading sectors of size were O&G up 1.7%, Mobile (+1.2%), Health Care Equip (+1.2%), Life Insurance (+1.5)

Underperforming sectors included REITS (-0.7%), F&D Retail (-0.2%) and Utilities (-0.2%)

GBP down 0.8% on USD and EUR. Gold flat, Silver down 0.3%, copper down 1.5%

Welcome to runprofits.com

Site is available to test users . You can register to use the site for free. Help and how to guides available by October 18.

Financial Week Ahead 17-23 Sep 2018

Companies Reporting

Over 60 companies reporting this week, most of them AImers

FTSE 100 - BAB, KGF and SMIN

FTSE 250 - DCG, OCDO, SGC, KIE

AIM All - 39 including CAML, QXT, SFE, CALL, EYE, FST, BGO, KWS

Economic Announcements

Wed - UK CPI, PPI, RPI Inflation figures

Thurs - Retail Sales UK

Fri - UK public sector borrowing

Full details for each day and weekly, monthly overview in Calendar Events

UK Markets Narrative Fri 14 Sep 18 EOD

Outperforming sectors included A&D (+2.2%), Construction (+1.8%), FS (+3.8%) and Mining up 1%

Utilities and electricity continued to underperformed with SSE losing another 3%. Tobacco closed down again by 0.7%

AIM was flat while the TechMARK closed up 0.6% driven in the main by the Pharmas rallying especially OXB

Oil has pulled back significantly from its recent touch on $80 owing to dissipating fears of the severity of Florence and it impact on US oil producers.

In the metals, copper took a break from its recent streak to close down 1% while iron ore gained almost 0.8%. Both gold and silver were down on the day as inflation fears seem muted

GBP touched $1.31 today before pulling back to close down almost 0.25%

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Wed 12 Sep 18 EOD

Today’s standout sector was Tobacco rallying almost 6% from a very oversold position (close to a bear correction of almost 20%). Mining came bouncing back rising 2.3% cheered by a sharp rebound in copper, zinc and many of the base metals rising over 2% on the day

An early rally in oil also lifted the O&G sector while T&L and Pharm also participated in today’s rally

Banks have continued to sell-off closing down 0.3% on the day while Insurance, Media and Utilities were all in the red with SSE falling over 8% on a profit warning

Oil closed up 0.4%, copper up over 2.5% and GBP flat against USD at $1.30

Despite today's rally all of the major indices remain bearish and below all moving averages with the exception of AIM which still above is 100 and 200 MAs.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Mon 10 Sep 18 EOD

Bullish comments from Barnier on Brexit helped to boost GBP which rallied above the significant $1.30 level: this also marks a close above the 50MA for the first time since April 2018. If this holds over the next few days then the worst could be over for sterling for now which will put pressure on the FTSE 100

While the UKX and NMX closed flat on the day, the MCIX rallied 0.4% while AIM closed down 0.2% and the TechMARK flat on the day

None of the price action today changes the overall bearish tone of the markets: the lack of any relief rally today may well be ominous and a preface to more selling to come

Today’s outperforming sectors of significance were Household and Home construction (+0.8%), Media (+0.5%) and Personal Goods (0.4%)

Mining continues to sell-off down 0.65% today and over 11% in the past month: , Tobacco lost an additional 0.7%

Looking across the sectors shows a sea of red across all timescales with most sectors having dropped below their 200MAs: only Pharm, Media and Support Services are clinging to their 200MA in the top 10 sectors

Failing a significant rally in the next couple of days, the most likely direction of travels seems to be downward with a bias to the short side

Brent rallied 0.5% on the day with the metals mostly flat on the day

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Thurs 06 Sep 18 EOD

Today’s selling was a continuation of the bearish sentiment evident across the UK and European major indices. The UKX closed the day down 0.9% and close to its lows on the day while the NMX sold-off by 0.8%. The MCIX fared marginally better at 0.6% while AIM bucked the trend rallying 0.35% aided by the likes of FDEV rallying 14% while HZD gained 8% and TAP 6%

The TechAMRK lost over 0.8% with the biggest loser being GNS down almost 7% with SPT and MCGN down 3%

In terms of sectors, the biggest loser were Mining (-2.3%), O&G (-1.5%) and Pharm (-1.5%) and Banks (-1.3%)

Defensive sectors all posted gains including Utilities (+1.8%), Comms (+0.7%) and Construction (+0.7%)

Brent reversed heavily during the day from posting a pop by 0.3% to closing the day down almost 1.5%

GBP rallied against USD gaining 0.2% and approaching the $1.30 level

Neither the fall in oil nor the rally in GBP can offset the wholesale selling across the major indices. September is often a poor month for equities as traders return from holidays.

UK Markets Close Tues 04 Sep 18

With only Banks, Electricity and Beverages moderately in the green: the UKX and NMX ended the day down over 0.6% reversing much of yesterday’s gains and closing below the 200Mas again

The TechMARK closed down almost 0.9% with SGE down 2%, AZN -1.8%, AVV -1.9%

AIM closed moderately in the green while Brent continued to rally up 0.4%.

GBP closed down over 0.4% against USD but this failed to boost the major indices

UK Markets Narrative Fri 14 Sep 18 EOD

Outperforming sectors included A&D (+2.2%), Construction (+1.8%), FS (+3.8%) and Mining up 1%

Utilities and electricity continued to underperformed with SSE losing another 3%. Tobacco closed down again by 0.7%

AIM was flat while the TechMARK closed up 0.6% driven in the main by the Pharmas rallying especially OXB

Oil has pulled back significantly from its recent touch on $80 owing to dissipating fears of the severity of Florence and it impact on US oil producers.

In the metals, copper took a break from its recent streak to close down 1% while iron ore gained almost 0.8%. Both gold and silver were down on the day as inflation fears seem muted

GBP touched $1.31 today before pulling back to close down almost 0.25%

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Thurs 13 Sep 18 EOD

The poorest performing sectors of note were Tobacco (-2%), Gen Retail and Media both -1.3%, Personal goods (-1.2%) while Pharm, A&D and O&G all underperformed the main index

AIM was relatively flat down -0.13% while the TechMARK also outperformed the main indices down only 0.35%

Oil also gave back 1.4% today although copper continued to rally.

The weakness in USD has given cheer to the US equity markets, this may translate to the UK and Europe tomorrow but for now the outlook remains muted for the main indices all of which remain below their 8,21, 50, 100 and 200 day moving averages. More green shoots are needed before taking anything other than strongly outperforming longs on an RSI basis

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Wed 12 Sep 18 EOD

Today’s standout sector was Tobacco rallying almost 6% from a very oversold position (close to a bear correction of almost 20%). Mining came bouncing back rising 2.3% cheered by a sharp rebound in copper, zinc and many of the base metals rising over 2% on the day

An early rally in oil also lifted the O&G sector while T&L and Pharm also participated in today’s rally

Banks have continued to sell-off closing down 0.3% on the day while Insurance, Media and Utilities were all in the red with SSE falling over 8% on a profit warning

Oil closed up 0.4%, copper up over 2.5% and GBP flat against USD at $1.30

Despite today's rally all of the major indices remain bearish and below all moving averages with the exception of AIM which still above is 100 and 200 MAs.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Tues 11 Sep 18 EOD

Other notable sectors that caught a bid today included Services, Personal Goods and Pharm all ending the day in the green.

However, Banks, T&L, Tobacco and Media all joined Mining in closing firmly in the red today

Chart patterns across the UKX, NMX and MCIX all signal a reversal is now due so a rally is to be expected in the next few days from fairly oversold conditions.

AIM closed down -0.3% while the TechMARK ended the day in the green up o.2%

GBP continues to hover around the $1.30 level which has proven to be a magic number over the past few months. With today’s unemployment figures combined it wage increase and a firmer GDP from yesterday, the path for another rate rise does seem set for later in 2018. That combined with more dovish rhetoric for the EU on Brexit would suggest that GBP is set to rally further

In other commodities, copper is down on the day as is iron ore and all the base metals. Neither gold nor silver can seem to catch a sustainable bid in the face of the strong dollar and trade tensions. Unless these conditions change, the mining sector remains too uncertain on any trading horizon until more clarity on macro conditions is available.

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Mon 10 Sep 18 EOD

Bullish comments from Barnier on Brexit helped to boost GBP which rallied above the significant $1.30 level: this also marks a close above the 50MA for the first time since April 2018. If this holds over the next few days then the worst could be over for sterling for now which will put pressure on the FTSE 100

While the UKX and NMX closed flat on the day, the MCIX rallied 0.4% while AIM closed down 0.2% and the TechMARK flat on the day

None of the price action today changes the overall bearish tone of the markets: the lack of any relief rally today may well be ominous and a preface to more selling to come

Today’s outperforming sectors of significance were Household and Home construction (+0.8%), Media (+0.5%) and Personal Goods (0.4%)

Mining continues to sell-off down 0.65% today and over 11% in the past month: , Tobacco lost an additional 0.7%

Looking across the sectors shows a sea of red across all timescales with most sectors having dropped below their 200MAs: only Pharm, Media and Support Services are clinging to their 200MA in the top 10 sectors

Failing a significant rally in the next couple of days, the most likely direction of travels seems to be downward with a bias to the short side

Brent rallied 0.5% on the day with the metals mostly flat on the day

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Narrative Fri 07 Sep 18 EOD

Mining (-1.7%) is yet again the underperforming sector which seems to be signalling more systemic global effects are in play. This is amplified by the developing markets economies crises: all are casualties of both a strong dollar and reduced liquidity as monetary policy across the globe adjusts and tightens.

Banks were also off almost 1.2% while O&G closed down 0.9%

The TechMARK managed to close the day in the green up 0.3%, the only UK index to close up.

Of the few green shoots in today’s sea of red were Mobile (+0.7%) ,A&D (+0.5%), Health Care Equip (+2.2%) with Software up over 1%

Oil closed down on the day by 0.7%, GBP up and the metals mixed: copper up 0.3% but gold down reflecting the stronger dollar. Silver rallied by 0.7% which, combined with a partial recovery in copper and iron ore, may be early signals that the worst is over for the miners. This is in turn would be bullish for the UKX and help shift market sentiment which is currently maudlin

Daily Short Interest Report

Daily Sectors and Shares Report

Welcome to runprofits.com

Site is available to test users . You can register to use the site for free. Help and how to guides available by October 18.

UK Markets Narrative Thurs 06 Sep 18 EOD

Today’s selling was a continuation of the bearish sentiment evident across the UK and European major indices. The UKX closed the day down 0.9% and close to its lows on the day while the NMX sold-off by 0.8%. The MCIX fared marginally better at 0.6% while AIM bucked the trend rallying 0.35% aided by the likes of FDEV rallying 14% while HZD gained 8% and TAP 6%

The TechAMRK lost over 0.8% with the biggest loser being GNS down almost 7% with SPT and MCGN down 3%

In terms of sectors, the biggest loser were Mining (-2.3%), O&G (-1.5%) and Pharm (-1.5%) and Banks (-1.3%)

Defensive sectors all posted gains including Utilities (+1.8%), Comms (+0.7%) and Construction (+0.7%)

Brent reversed heavily during the day from posting a pop by 0.3% to closing the day down almost 1.5%

GBP rallied against USD gaining 0.2% and approaching the $1.30 level

Neither the fall in oil nor the rally in GBP can offset the wholesale selling across the major indices. September is often a poor month for equities as traders return from holidays.

UK Markets Narrative Wed 05 Sep 18 EOD

AIM has finally taken a breather from its relentless upward climb closing down 0.6%. The TechMARK also closed down almost 1% and testing its 200MA before bouncing into the close.

Of the Top 10 sectors, Banks, Mining, Tobacco and Life Insurance are below all of their short medium and long-term MAs including their 200MAs with Mining and Tobacco almost 10%b below their 200MA

While some relief in the selling may be on the cards, the overall timbre of the markets has turned bearish

Pharmaceuticals and Support Services remain the most resilient sectors in the top 10 while Non Life Insurance, O&G Services, Auto Parts and leisure Goods remain the most bullish

GBP reversed sharply on USD today on news that Germany may be more open to a Brexit deal. Brent crude closed down almost 1% on the day which added to the UKX woes while metals were mixed with iron ore and copper rallying modestly

UK Markets Close Tues 04 Sep 18

With only Banks, Electricity and Beverages moderately in the green: the UKX and NMX ended the day down over 0.6% reversing much of yesterday’s gains and closing below the 200Mas again

The TechMARK closed down almost 0.9% with SGE down 2%, AZN -1.8%, AVV -1.9%

AIM closed moderately in the green while Brent continued to rally up 0.4%.

GBP closed down over 0.4% against USD but this failed to boost the major indices

UK Markets Close Mon 03 Sep 18

The UKX was also boosted by a rise in oil prices with Brent up 0.6% at pixel time. The NMX followed suit with the UKX closing up 0.8%. Both these indices recapture their 200MAs which is a positive result though they are firmly below their 100 and 50 MAs and their 21 and 8 EMAs so caution should be taken. That the 200MA has been recaptured may be significant although volumes were light. Confirmation of any rally would be needed in the next few days with prices closing above the 21EMA ideally on two consecutive days.

The MCIX by contrast remain better behaved following the 8 EMA and closing flat on the day unmoved by GBPs episodic spasms. AIM rallied 0.3% keeping tis upward trajectory though forming a doji on the day which may be signalling a pause in its rally

The TechMARK had a strong day up 0.9% buoyed in the main by SN, MCRO and a rebound in SGE

Today’s leading sectors of size were O&G up 1.7%, Mobile (+1.2%), Health Care Equip (+1.2%), Life Insurance (+1.5)

Underperforming sectors included REITS (-0.7%), F&D Retail (-0.2%) and Utilities (-0.2%)

GBP down 0.8% on USD and EUR. Gold flat, Silver down 0.3%, copper down 1.5%

UK Markets Close Fri 31 Aug 18

The FTSE 250 closed flat on the day while AIM rallied 0.2%. These markets are relatively sheltered from GBP and international trade concerns which is probably reflected in their more bullish stances.

The TechMARK closed down over 1% in the main due to SGE’s tumble: XAAR by contrast recovered almost 9% on yesterday’s 30% drop. CCC, SDL and VEC all added to the index’s weakness

Oil continued to rally up a further 0.3% making a 5-day gain of over 4%. Copper and Iron ore closed down on the day

GBP pulled back against USD and is down 0.4% at pixel time holding the 1.29 level: GBP is up against EUR by 0.2% but remains unconvincing against the downward channel

UK Markets Close Thurs 30 Aug 18

The MCIX yielded only 0.2% supporting the notion that it is GBP strength that is weighing on the major indices.

AIM rallied 0.3% bucking the trend of the other indices

The TechMARK sold-off the heaviest down 0.8% with almost all of this decline owing to Xaar losing 30% on the day on a profit warning. CCC and OXIG were also down 2% on the day

Oil continues to rally and looks set to retest the $80 level: this lifted the O&G Services sector (+0.8%) and the O&G Producers (+0.4%). These were among the few green sectors in an otherwise sea of red today . VOD dropped over 3% taking down the Mobile Sector while Banks, Tobacco and Mining all underperformed the index

UK Markets Close Wed 29 Aug 18

The boost to GBP reflected in a sell-off in FTSE 100 and the 350 down 0.7 and 0.6% respectively slipping back below their tightly aligned moving averages

AIM pulled back just 0.25% while TechMARK lost 0.5%

The biggest sector moves were in O&G Services -2.8%, F&D Retail -2.1%, Ind Trans -2% with most sectors down on the day. Only Food Producers (+0.8%), Software (+0.6%) and REITs (+0.4%) were up on the

Brent rallied almost 1% with day copper and gold flat on the day

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Close Tues 28 Aug 18

The move was lead in the main by Miners (+2.1%), FS (+1.4%), Personal Goods (+1.4%) with almost all sectors in the green on the day

Only Food Producers (-1.1%), Tobacco, Construction, O&G and Mobile closed down on the day

AIM broke out strongly up over 1% with TechMARK up 0.6%.

Brent was up 0.3% but may be at the top of the sideways channel and may well pull back from here

GBP lost ground against USD continuing tis downward trajectory and making a new low for the year against EUR

Copper continues to base while iron ore was flat on the day

UK Markets Close Fri 24 Aug 18

NMX continues to roll sideways with lower daily volumes closing today up 0.2% bolstered by the US making another new high with the S&P

The MCIX rallied a mere 0.1% but may well be preparing to breakout north from a bullflag in place since the 12 June high: next week may well prove pivotal

AIM was flat on the day but remains bullish on all time scales and is the outperformer in 2018 for the UK. The brief visit to the 50MA on 21 Aug has been received with strong buying

The TechMARK continues to forge ahead adding another 0.4%: this index has been clinging to its 50DMA since late June and looks set to break north. Given the leadership role of technology this may well be bullish the overall markets

Oil remains range-bound in its sideways channel and look set to revisit the top channel line around $78 . If this is broken then new highs above $80 would be expected

GBP continues to be subdued by USD with price action upper bound by the 21EMA since July. A close above the 21EMA would be bullish and may signal a relief rally. By contrast GBP made a new low against Euro sinking to €1.10 today

Gold may well have bottomed making a strong engulfing up thrust today rising almost 2% to close above $1200. Silver made an even stronger rebound up almost 2.5%

Iron ore seems to be bottoming while copper staged a recovery

The relative dollar weakness and strength in commodities and metals helped the Mining sector to recover over 2% today though the sector remain pretty beaten up down almost 10% ytd

O&G services continues its rally up another 1.2% making a 5 day rally of almost 15%: O&G producers also rallied along with Pharm and T&L

The losing sectors today included Tobacco (-3%), Utilities and Household/Construction

UK Markets Close Thurs 23 Aug 18

Flat day across all major markets with only AIM rallying by over 0.8%

The main indices are bearish across short, medium and long timescales and remain below 50 and 100 MAs with 200MAs checked recently

Given it is low volume during the holidays, the return to full volume over the next week or two will confirm the direction but currently this is firmly downwards

Outperforming sectors included O&G Services (+1.6%) for the third day running rising over 12% in 5 days and almost 20% in the past month. O&G was up 0.6% with support services up 0.5%

Underperforming sectors included Tobacco down another 1.4%., Pharm (-0.7%) Mining (-0.6%)

Oil pulled back marginally from the recent large moves as did cable

UK Markets Close Wed 22 Aug 18

NMX closed flat up less than 0.1% while the MCIX was also unchanged

AIM rallied a mere 0.2% while the TASX was similarly flat

In sectors O&G Services stood-out rallying another 5% as WG continued to power higher. Mining, O&G, F&D retail all rallied close to 1%

Underperforming sectors included Utilities, A&D, Tobacco and Food Producers

Today’s rallying sectors were driven by improvements in commodities with Brent up almost 2.5% at pixel time and base metals holding recent gains

GBP was flat against USD on the day

Daily Short Interest Report

Daily Sectors and Shares Report

UK Markets Close Fri 10 Aug 18

Mining performed the worst of the major sectors off over 2%: A&D, Telecoms, O&G Gen Retail and FS all suffered more than 1% losses

Only Utilities, Ind Transportation and Leisure Goods (GAW) showed any green today

GBP is now at the 1.28 level against USD, a level not seen in over a year. Clearly the markets are concerned on Brexit and several other macro concerns including trade wars and the Turkey-European jitters. However, light volume and empty trading desk also contribute to volatility at this time of year

UK Markets Close Thurs 09 Aug 18

NMX sold-off today following yesterday’s up thrust dropping -0.35% but rallying off intraday low: volume was lighter than usual reflecting the holiday period.

The drop was largely architected by O&G (-1.8%), Bevs (-1%) A&D (-0.6%) with Mobile and Household Good also contributing to the fall.

Outperforming sectors of note included T&L (+0.6%), Gen Retail (+0.7%), F&D Retail (+0.8%)

By contrast, MCIX rallied 0.2% and AIM +0.6% while the TechMARK pulled back from recent gains losing 0.3%.

Oil was flat on the day as was GBP against USD

UK Markets Close Tues 07 Aug 18

UK Markets Close Mon 06Aug 18

Gold and silver sold-off as did copper retracing may of its recent gains to recheck support around the $2.70 mark

UK Markets Close Fri 03 Aug 18

UK Markets Close Thurs 02 Aug 18

Markets continue in sell mode for the second day of August with Mining sliding another 3%. Some huge losses on earnings from the likes of FXPO (-20%), Kaz (-30%) while the UKX miners were all down more than 3% except BLT (-2.2%). The sea of red was pretty widespread with Insurance down over 2% and most of the major sectors down over 1% including O&G, T&L, BanksThere were a few green shoots in the mix with A&D up over 2% helped by RRs rally of over 6%. SGE helped to list Software by 1% while Utilities staged a bit of of a comeback presumably on a safety playThe MCIX suffered a larger loss down almost 1.4% and closing on its lows which is foreboding. Hit by the junior miners like KAZ and FXPO there was little shades of green across a very red heatmap. ISAT, TCG, MAB, EMG and GNK all lost around 5% or more on the day AIM was off 0.5% whilst the TechMARK suffered the same Brent rallied almost 1% today while the base metals continued to sellIn terms of narrative, BoE raised rate to 0.5% but maintained a steady-as-she-goes stance on further rises: this softened GBP which had front run a more hawkish outlook resulting in GBP dropping 0.7% to revisit the $1.30 level. Give the ferocity of selling over the past few days, a relief rally tomorrow would not be unsuprising

Short Interest

Sectors and Shares

UK Markets Close Wed 01 Aug 18

UK Markets Close Tues 31 July 18

UK Markets Close Mon 30 July 18

UK Markets Close Fri 27 July 18

A day in green across all the UK markets with a bounce back in Household Goods, Telecoms , Mining and O&G helping to lift the major indices

Lagging sectors included Tobacco, Gen Retail and Construction

Oil was flat on the day while copper continued to rally

In currencies GBP held solid against USD into next week's BoE interest rate decision

Short Interest

Sectors and Shares

UK Markets Close Thurs 26 July 18

UK Markets Close Wed 25 July 18

NMX gave back most of yesterday’s gains dropping 0.63% where Life Insurance (-25), Travel and leisure (-1.5%) while Mining Banks and Mobile Comms all lost over 1%.

Outperforming sectors included |Tobacco (0.25%), beverages (+0.4%), F&D Retail (+0.55%)

Wizz Air, INDV and FRES all sank 7% or more on poor results

Meanwhile AIM popped over 1% making new highs for the decade. TechMARK pulled back almost 0.9% weighed down by SXS, BA and BTG

Brent closed flat while copper continued to rally modestly which may be signalling and easing on trade tariff concerns.. GBP was flat on the day

UK Markets Close Wed 18 July 18

Another day in the green for all UK markets with the resource sectors fighting a comeback and lifting the UKX and NMX. GBP’s drop was a significant driver in the rally which followed a lower than expected inflation reading at 09.30 …casting an interest rate hike in doubt for August .

Mining did a lot of the lifting rallying 1.7% while Insurance (+1.4%) Financial Service and Banks also outperformed the index along with Beverages, and Tobacco

This now places the NMX back at the top of the channel line in place since late May and closing back above the 50MA. This may well signal a break out and a move further north to new highs: the next few days maybe be pivotal. If GBP weakness persist then the path of least resistance is higher from here

The domestic focused MCIX rallied above tis 50DMA but closed just shy of it: one to watch

Meanwhile AIM continued to power on and probed new highs not seen since 2007

The TechMARK also had a good day and is firmly in breakout mode with A&D and Software powering the index higher

Oil staged a further recovery which relieved the oilers and at time of writing is up almost 2% on the day. Metals remain moribund though relatively becalmed compared to the recent falls

UK Markets Close Tues 17 July 18

Markets took a more bullish tone today with the NMX staging a recovery and an “inside day” which may signal more rallying to come. A lower support line in evidence now suggest that the consolidation period of the past few weeks may be drawing to a close with a potential move north. The NMX, UKX and MCIX all closed above their 8 and 21 EMAs today with almost every market including the AIM and the TechMARK moving by an almost identical 0.35-0.4%. Typically, two or more closes above the 8 and 21 EMS can be taken as a bullish sign. That said, all the major UK indices remain below their 50DMAs so a recapture of this important level with reasonable volume would be a welcome signal. That should eb achieved relatively easily given how close price has been tracking the 50DMA over the past few weeks.

In terms of sectors moving the markets, the outperformers today were Mining (+1.4%) , Beverages (+1.5%) with Pharm (+0.9%) and O&G (+0.5%) outperforming the indices. O&G services (-1.5%) and Tobacco (-1.3%) were among the underperformers with Construction, Telecoms, banks and Food Producers.

Oil had a brief bounce today while GBP weakened against USD which strengthened against the EUR as well. Yen is bucking the trend and moving to test 2018 highs

Metals have continued to sell with gold falling over 1% today testing lows not seen since July of last year

UK Markets Close Mon 16 July 18

MCIX fared better on the day down 0.2% buoyed in part by Construction and Homebuilders

Both AIM and the TechMark closed down around 0.4% : MCRO, SHP and SN weighing heavily on the tech index

With Banks, Mining, Life Insurance and Financial Services bearish across 8 to 200 MA timescales; and with Oil and Gas looking set to follow, the overall sentiment is one of risk-off. Gold has remained stubbornly low, often a sign of flight to safety while the VIX trundles along around 12 indicating market participants see little to be of concern.

In currencies GBP close flat on the day while the JPY pared some of its recent gains against USD but remain in a break-out move which may be significant. The slew of inflation data this week across the UK , EU and JP combined with retail sales from many of the major economies should make for some volatility in the major pairs

UK Markets Close Fri 13 July 18

AIM rallied a further 0.5% and remains the most bullish UK index although it may be showing signs of fatigue with a double top to the June highs. Similarly bullish is the TechMARK which rallied a further 0.4% and may be setting up for a breakout north. This would be an overall bullish sign for all indices

GBP is remains in a sideways consolidation against USD as markets digest the recent economic good news with the dark clouds of Brexit uncertainty. While the overall trend is firmly downwards, a relief rally is not off the table.

Brent recovers somewhat today but remains bearish in the short to medium terms with the most likely direction being downwards. This is likely to be negative the O&G and Oil services sectors and may weigh on the UKX. All of the metals are a sea of red across all major timescales which will weigh on the miners . This is unlikely to change unless trade tariff tremors subside.

The rally in the JPY suggest an element of risk-off as the Yen breaks out from a downward channel that has been in play since 2015: this may be a signal of more weakness to come.

Financial Week Ahead 17-23 Sep 2018

Companies Reporting

Over 60 companies reporting this week, most of them AImers

FTSE 100 - BAB, KGF and SMIN

FTSE 250 - DCG, OCDO, SGC, KIE

AIM All - 39 including CAML, QXT, SFE, CALL, EYE, FST, BGO, KWS

Economic Announcements

Wed - UK CPI, PPI, RPI Inflation figures

Thurs - Retail Sales UK

Fri - UK public sector borrowing

Full details for each day and weekly, monthly overview in Calendar Events

Daily Analysis UK Markets Close Thurs 12 July 18

Sectors outperforming today included Software (+2.7%) driven mainly by a 10% rise in CCC, Pharm (INDV +8%, AZN +3.5%), while Media T&L, A&D , Tobacco and Bevs all outperforming the index and rising more than 1%.

Oil sank over 1% following yesterday’s almost 6% drop which depressed O&G while metals continues to languish with copper losing over 1%: this weighed on Mining. The resource sectors have tended to be a barometer of trade tensions with mining companies reacting dramatically to increased threats. Oil may well have double topped on the $80 this may depress oilers if continued weakness is seen. Dr Copper is not yet signalling and end to the recent softness. A rally in copper would support the bullish sentiment

UK Markets Close Wed 11 July 18

What a difference a day can make, trade war escalations now look set to get beyond sabre rattling to much more damaging levels as Trump threatens hundreds of billions of goods in line for tariffs from China while simultaneously alienating Germany as “under Russian control”. The inherent stability of one individual seems to have echoed in global markets with European and UK markets ending heavily in the red. The NMX and UKX sank by over 1.2% owing mainly to heavy losses in Mining (-3.6%) , O&G (-2.5%) with losses across most sectors.

The dramatic nature of today’s losses may well call into question the nascent summer rally: price action over the next few days will clarify

Some stand-out losses on the day include INDV down almost 35% and MCRO down almost 10% on the day.

AIM fared best on the day off only 0.5%. TechMARK was off over 1.2%

Oil tumbled almost 3% while GBP was flat on the day .

Copper is staging a relief rally which may well auger well for overall market health. However the huge sways in commodities are direct echoes of trade tensions and their global impact

Upcoming Events Week 33: 13-17 Aug 2018

FTSE 100 reporting this week are ANTO, ADM and KGF. 11 Mid caps report including CKN. BBY. HOC and KAZ. In small caps there are 7 reporting including MNZS, LOOK and ALM

In economic news , UK updates on employment on Tuesday while GER has CPI and ZEW numbers. UK inflation on Wed may well impact GBP and give clues on further interest rate pressures

UK retail sales will be keenly watched on Thursday and EU inflation is reported on Friday.

In the US, reports on housing starts, retail sales and the CCI

More details in Calendar Events