Pre Market 07:30 FTSE 100 Testing Recent Highs. Copper at 7 Year Highs. Oil Up as Resource Sectors Rally

Futures call for a paring of some of yesterday's gains with The FTSE 100 set to open down 20 points around the 6440 level. America closed flat to positive while Asia was similarly flat.

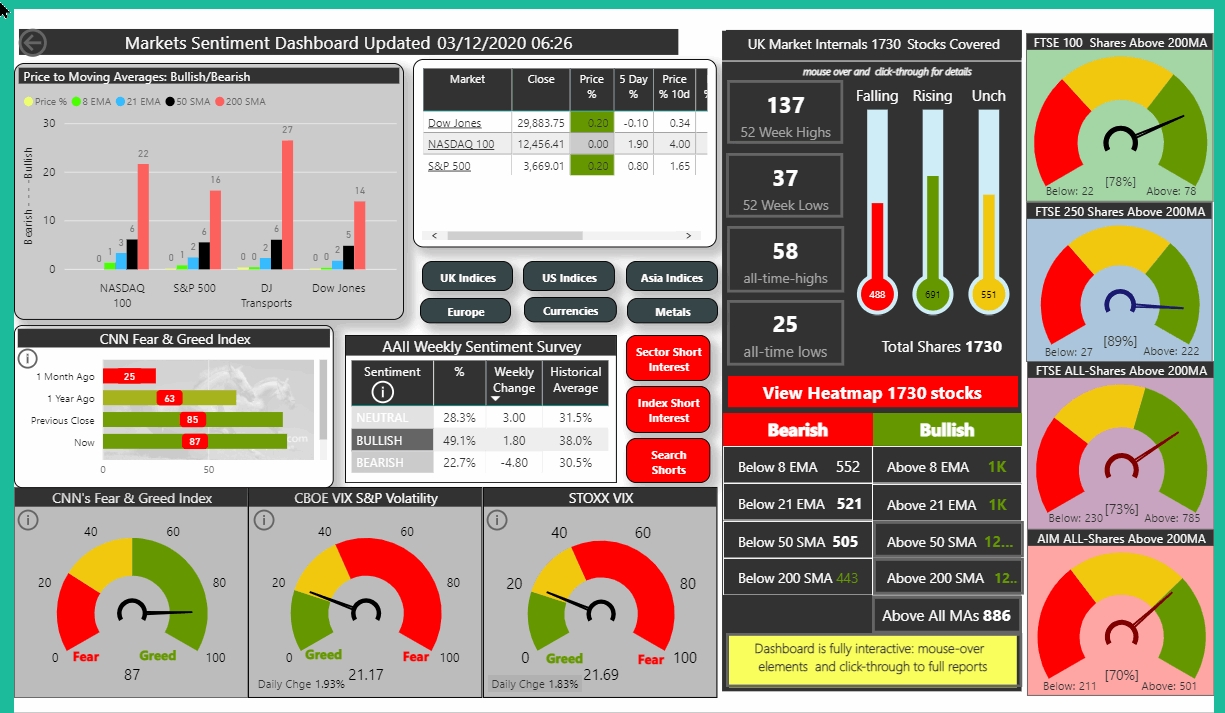

Sentiment is in full risk-on mode with the F&G index firmly in extreme Greed at 87 while the VIX hovers around 21. The AAII sentiment indicator is skewed to almost 50% bullish from a long term average of 38%

Copper has hit a 7 year high as has iron ore while oil rallies north of $48 lifting all of the resource sectors. Widening spreads in short and long term bonds are suggestive of increasing interest rates which combined with the changes in commodity and resource sectors is suggestive of inflationary pressures. Given the enormity of quantitative easing carried out globally to salve the pandemic's economic wounds this should not be too surprising.

The FTSE 100 opened slightly negative yesterday but rallied to close up 1.2%. It is tempting for punditry to explain the rally on the news that the vaccine rolls-out next week: both literally from the Belgian Pfizer plant as well as the programme to inoculate the British public. That the index was actually lifted by resources stocks in Mining and Oilers as well as Banks doesn't follow that narrative nor that the reopening favoured sectors like Travel and Leisure or Gen Retail were neutral to red. The FTSE 250 spent most of the day in the red but made a recovery to close flat while the AIM All-Share didn't do much more than a +0.2%. Both these indices should have been basking in the vaccine afterglow. If Mr Market follows his typical behaviour he may well react by selling on this news: it's kind of his thing to be predictably unpredictable. Both the FTSE 100 and the FTSE 250 are hanging on their previous highs and seem to be running out of momentum: the prospect of double top reversal does look more likely unless these can get their momo-mojo back. Potential catalysts included a positive Brexit resolution, US fiscal stimulus thought given the November rally, markets do seem priced for perfection

19 UK Companies Reported by 07:30